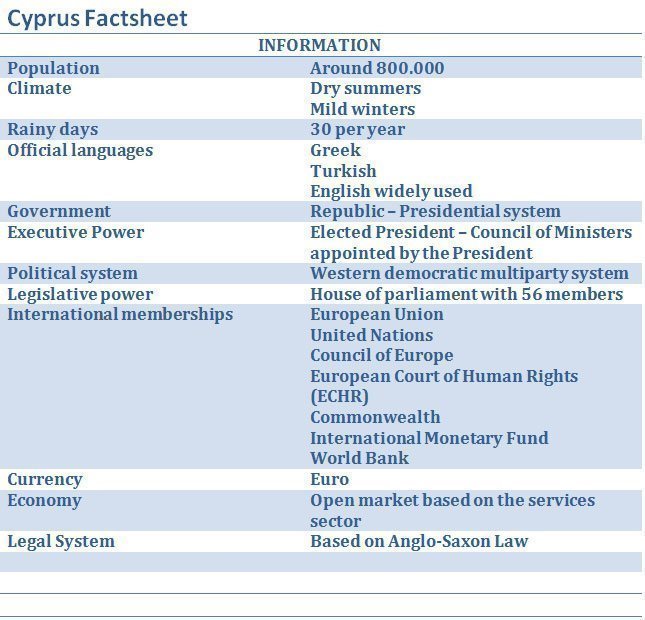

| WHY CYPRUS |

| “Operating through a company registered in Cyprus can significantly reduce the tax liability of the business and the ultimate shareholders, thus increasing the net return on the investment.” |

Country Tax Profile

Location

Cyprus is an island lying at the southeastern corner of the Mediterranean. It is the third largest island in the Mediterranean. The geographical position of the island played a significant role in rendering it into an international business center, as it is in the crossroads of three continents (Europe, Asia, Africa) and the Middle East.

Cyprus Companies incorporations

There are more than 225,000 companies registered in Cyprus, evidence of the attractiveness of Cyprus’ taxation system benefits and international investors’ confidence in Cyprus economy.

Banking System

The banking system in Cyprus is capable of providing fast and effective services worldwide. The system is under the supervision of the Central Bank of Cyprus (www.centralbank.gov.cy) which controls all businesses carried out by commercial banks and other financial institutions.

All financial institutions provide a wide range of services and they are all subscribers to the SWIFT system (Society for World Interbank Financial Telecommunications).

Cyprus Stock Exchange

The Cyprus Stock Exchange (CSE – www.cse.com.cy) commenced its operations since 1996. Towards the end of 2006 the CSE entered into strategic agreements with the Athens Stock Exchange (ASE), thus creating a joint forum for processing transactions. Today the CSE numbers around 130 listed companies. The official currency for transactions is the Euro.

On 29th March 2010 the Cyprus Stock Exchange launched a new market called the Emerging Companies Market (ECM). ECM is governed by a simplified regulatory environment, which has been specifically designed for the needs of small company listed in an EU stock exchange.

The market is considered to be a Multilateral Trading Facility that will operate according to the Regulative Decisions of the CSE.

The particular market is addressed to unlisted companies seeking for external funding and easy access to a secondary / alternative market that will save significant costs and promote the recognition and reputation of the companies at the same time. In addition to that there is no minimum share capital that must be dispersed to public along with no criterion for a minimum market capitalization.

Specific conditions for listing in the EMC market along with the procedure followed can be provided upon request through nominated advisors within our network of associates.

WHY CYPRUS

Operating through a company registered in Cyprus can significantly reduce the tax liability of the business and the ultimate shareholders, thus increasing the net return on the investment.

Cyprus has been a full member of the European Union since 2004 and adopted the Euro as its official currency since the beginning of 2008.

The strategic position and time-zone of Cyprus, enables comfortable connections between Europe, Middle East, Africa and Asia and make the island a natural hub for business and trade.

Cyprus is an established and reputable business and financial center supported by an advanced legal, accounting and banking system, highly skilled and multilingual workforce, excellent telecommunication systems and convenient year round flight connections.

In addition, due to the great numbers of international businesses already situated in Cyprus, there are outstanding networking possibilities for all of new entrants.

The local governments have traditionally been promoting Cyprus as an international business center, through the enactment of favorable tax laws, which are in full compliance with EU directives and the reduced paperwork and costs necessary to register a Cyprus company.

CORPORATE TAX PROVISIONS

Corporate Tax Rate

Trading profits of a Cyprus tax resident company are taxed at the rate of twelve and a half percent (12,5%), one of the lowest corporate income tax rates in Europe. Business profits of non-resident companies are tax free.

Cyprus Tax Resident

A company is considered to be tax resident in Cyprus, if its management and control is exercised in Cyprus.

Interest Income

There are two types of taxes that may apply to interest income earned by a Cypriot company: income tax at 12,5% levied on interest derived, less any allowable expenses or Special Defence Contribution (SDC) at 30% applied to gross interest income. Interest earned by a Cypriot tax resident company derived in the ordinary course of business or closely connected thereto is only subject to income tax. Interest income by all other companies is subject to SDC.

Dividends

Dividends Received from Abroad

Dividends received from abroad are tax exempt unless both of the following conditions are not satisfied, in which case they are taxed to Special Contribution for Defence (SCD) at 17%:

(1) The company paying the dividend must not engage directly or indirectly more than 50% in activities which lead to passive income (non-trading income), and

(2) The foreign tax burden on the income of the company paying the dividend is not substantially lower than the tax burden in Cyprus (an effective tax rate higher than 5% in the country paying the dividend satisfies this condition.

A tax credit will be afforded according to the Double Taxation Agreements concluded by Cyprus. In the absence of a Double Taxation Agreement, Cyprus unilaterally affords a credit for the foreign tax paid on such income. For dividends received from EU Member States the underlying tax credit is also available.

Royalties

There is an 80% exemption on the net income generated from the utilization of patent, trademark or any other intellectual property (IP) rights, given certain conditions and criteria. This exemption results in an effective tax rate of 2,5% from the utilization of Cyprus registered IP.

Gross amounts of royalties from sources within Cyprus by a company which is not a tax resident of Cyprus are liable to 10% withholding tax at source. If the intangible property right, however, is granted to a Cyprus company for use outside Cyprus, then there is no withholding tax and the corporate rate is applied only on the profit margin left in the Cyprus Company.

Trading In Titles

Gains from trading and disposal of securities are tax free. The term ‘Titles’ includes:

- ordinary and preference shares;

- founder’s shares;

- options on titles;

- debentures;

- bonds;

- short positions on titles;

- futures / forwards on titles;

- swaps on titles;

- depositary receipts on titles;

- rights of claims on bonds and debentures;

- index participations (if they result in titles);

- repurchase agreements or Repos on titles;

- participations in companies; and

- units in open-end or closed-end collective investment schemes such as Mutual Funds, International Collective Investment Schemes (ICIS) and Undertakings for Collective Investments in Transferable Securities (UCITS).

Foreign Permanent Establishments (PE)

The profit of a foreign PE of a Cyprus Holding company is exempt from corporate tax in Cyprus, if one of the following two conditions is satisfied:

(1) The PE must not engage more than 50%, directly or indirectly, in activities which lead to passive income, or

(2) The foreign tax burden imposed on the PE must not be substantially lower than that in Cyprus.

Group Relief

Group relief is allowed for at least seventy-five percent (75%) group structures and is applicable only on yearly results if claimants are Cyprus tax resident companies and are members of the same group for the whole tax year. Losses incurred from business carried outside Cyprus are allowed as a deduction against other taxable profits generated by the Cyprus Company.

Losses

Tax losses are carried forward for five years.

OTHER TAXES

Withholding Taxes

There are no withholding taxes on payments to non-tax resident persons (companies or individuals) in respect of dividends and interest.

Capital Gains Tax (CGT)

Capital gains are not included in the ordinary trading profits of a business, but instead are taxed separately under the CGT Law. Capital gains from the sale of immovable property situated in Cyprus as well as from the sale of shares in companies (other than quoted shares) in which the underlying asset is immovable property situated in Cyprus, are taxed at a flat rate of 20% after allowing for indexation. Capital Gains that arise from the disposal of immovable property held outside Cyprus or shares in companies which may have as an underlying asset immovable property held outside Cyprus, are completely exempt from capital gains tax.

Inheritance or Estate Taxes

There are no inheritance or estate taxes on shares held in a Cyprus company.

Wealth Taxes

Cyprus imposes no tax on wealth.

Stamp Duty

Stamp duty is enforced on written documents which deal with Cyprus situated property or matters that will be performed in Cyprus, irrespective of where the agreement is signed.

OTHER CONSIDERATIONS

No Thin Capitalization Rules

There are no thin capitalization rules in the Cyprus tax legislation. However, interest suffered on loans used for the acquisition of assets not used in the business is not tax deductible.

Transfer Pricing Legislation

The transfer pricing legislation in Cyprus follows the provision in the Income Tax Law, which requires transactions between ‘related parties’ to be in accordance with the ‘arm’s length principle’. The Cyprus tax legislation adopted the OECD model and guidelines to determine whether a transaction is at arm’s length.

Controlled Foreign Companies (CFC) Rules

Controlled Foreign Companies rules in Cyprus tax legislation and Cyprus companies are based on EU principles.

Exit Routes

The Cyprus Company offers an ideal exit route through a tax free sale of participations and own shares or the liquidation of the company and distribution of the proceeds completely tax free to the non-resident shareholders.

VAT

In accordance with the Cyprus legislation every corporation must be registered in the Value Added Tax (VAT) Register provided that they have an annual turnover exceeding 15,600 Euro. Voluntary registration is also possible.

Where the exclusive purpose of a holding company is the acquisition and holding of interest in shares in other companies, with the intention of deriving dividend income, such a company is not considered to be performing an economic activity for VAT purposes and consequently it does not have the status of a taxable person.

Companies which are not performing economic activities have neither the liability nor the right to register for VAT purposes and consequently they cannot claim input VAT. However, holding companies may be liable to register for VAT where, in addition to the holding of investments, they also have taxable or exempt activities such as:

• Supply management services at a consideration to subsidiaries;

• Supply finance to subsidiaries;

• Trade in shares i.e. purchase and sell shares on a frequent basis with the intention to profit from the fluctuations of the share price.

Where a holding company is registered for VAT purposes, it may claim input VAT on goods and services acquired in Cyprus and other EU Member States. The right to claim input VAT depends on which type of the holding company’s activities the acquired goods or services, directly or indirectly relate.

Reorganization Provisions

Cyprus legislation provides for a fully exempted reorganization of Companies procedures. Such reorganization may include any division, merger, partial division, transfer of assets, exchange of shares and redomiciliations. The same reorganization provisions apply in Cyprus and for all EU Companies or Cyprus Companies in other EU Jurisdictions under the European Union Merger Directive.

Advance Rulings

Advance rulings can be obtained from the Income Tax office upon request.

Re-Domiciliation of Companies

Re-domiciliation of any share capital in and out of Cyprus is permissible; however, the other jurisdiction’s legislation must also recognize such a possibility.

DOUBLE TAX AGREEMENTS(DTA)

Cyprus has currently concluded DTAs with more than 65 countries including the majority of the European countries, the United States of America, Canada, India, China, Russia and the C.I.S countries. The Cyprus treaty network covers more than 80% of the global GDP.

ESTABLISHING A COMPANY IN CYPRUS

Traditionally Cyprus was a territory with a growing business activity mainly as a station for international businesses. The means for such activities has always been the Limited Liability Company with shares.

Participation of non-Cypriots in a Cyprus Company

There is no requirement or licensing procedure for the participation of foreigners in a Cyprus company. Their participation in a company may be up to 100% of the shares and there are no conditions regarding the minimum amount they must invest in the capital of the company.

Company Registration Procedure

The procedure for the registration of a Company is relatively simple and it usually takes approximately 3-5 working days.

Name of the Company

The name of the Company must be approved by the Registrar of Companies. The word Limited must be inserted after the name of the Company (Limited or Ltd). 5- 7 working days are required for the approval of the name.

Names which have already been approved by the Registrar of Companies or are descriptive in general or names which can be reminiscent of particular words or geographical locations cannot be approved by the Registrar of Companies.

Names which are considered misleading or are associated to royalty such as “Royal, King, Queen, Crown or including the following words: Imperial, National, Commonwealth, Cooperative shall not be approved by the Registrar of Companies.

The names may be registered in any language using the Latin alphabet provided that the Registrar of Companies has been given the Greek or English translation.

Memorandum of Association and Articles of Association

The Memorandum of Association and the Articles of Association must be drawn by a local lawyer and is divided into two parts.

The Memorandum of Association, which includes the objects and the powers of the Company, the limited liability of members and the share capital. The Memorandum of Association must also include the following:

• The name of the Company

• The registered address of the Company which must be in Cyprus

• The share capital

• The names, addresses and description of the Shareholders together with the number of shares held by each one of them.

The Articles of Association which include the regulations for the internal administration of the company and the rights of the shareholders. The Articles of Association must also contain the following:

• The general meetings of the Company

• The voting rights of the members/shareholders

• The appointment, powers and competencies of the Directors

• The dividends

The Memorandum of Association together with the Articles of Association and all documents appointing the Directors, the Secretary and the Registered Office of the Company must be submitted to the Registrar of Companies who then proceeds with the registration of the Company.

Share capital

The share capital is expressed in euro (€) or any other currency of preference and is divided into shares of any value (usually €1 or any other currency).

The nominal capital is the total capital which the Company may issue to the shareholders.

The Paid up Capital is the part of the Nominal Capital issued to the shareholders and paid by them.

The Nominal and fully Paid up Capital has no legal requirements with respect to a minimum or maximum amount.

It is recommended that the minimum nominal share capital is €1,000. For particular types of companies, such as insurance companies, O.B.U’s etc., the Nominal and Paid up share capital allowed has a minimum requirement which is specified according to the type of the particular enterprise. The nominal and paid up share capital may be increased at any time with a special resolution of the shareholders of the company.

Shareholders

Every Private Company of limited liability with shares must restrict the number of its shareholders to a maximum of fifty (50) and a minimum of one (1) shareholder.

All shares are of nominal value and in the case of a private company it is prohibited to issue share warrants to the bearer. However, the owners who do not wish to appear as registered shareholders may appoint nominees who shall be acting on their behalf as registered shareholders. The actual ownership shall always remain with the beneficial owners of the shares. The nominee shareholders may be Cypriots or aliens.

Directors

The Law does not provide for any special requirements according to which the Private Company shall have more than one Director or that the Company must have local Directors. However, for a company to be considered as a tax resident of Cyprus (securing the address and the control of the company for tax purposes in Cyprus and for the smooth operation of the company in Cyprus), it is proposed that local Directors or alternate Directors are appointed.

The Secretary

The Company must have a secretary. The Secretary acts under the control and the instructions of the Directors, keeps under his/her control all legal documents of the company and carries out administrative duties which are not of executive nature.

Registered Office

Every Company must have a Registered Office which shall be its official address in Cyprus. The registration certificate must be posted in a prominent position in the premises and the legal books of the company must be kept there.

Bank Accounts

The Company may open a bank account with any Bank in Cyprus and in any currency. Furthermore, the company may keep accounts in any other country. The transfer of money may be carried out without any exchange restrictions.

Double Taxation Documents

Upon the establishment of the company and provided that all relevant conditions are complied with, it is possible to receive the relevant certificate from the Ministry of Finance of the Republic of Cyprus, which shall certify that the Registered Tax Address of the Company is in Cyprus. Such certificate may be obtained by the Directors of the Company after its registration with the tax authorities in Cyprus (Income Tax) and after obtaining the Tax Identity Number. Management Companies usually processes the registration through the tax authorities and the issue of the double taxation certificate immediately after the establishment of the Company.

Books of Accounts

Every company of limited liability must keep books of accounts. Such books must be kept at the registered office of the company.

Audit

The books of accounts of the Company must be audited at the end of each financial period by accredited accountants in Cyprus based on International Financial Reporting standards, as adopted by the EU.

Submitting an Annual Report to the Registrar of Companies

At the end of each year, companies are obliged to submit to the Registrar of Companies an annual report declaring the state of the Company. The annual report must be accompanied by the final accounts of the previous year. At the same time the annual tax return is submitted to the Inland Revenue Department.

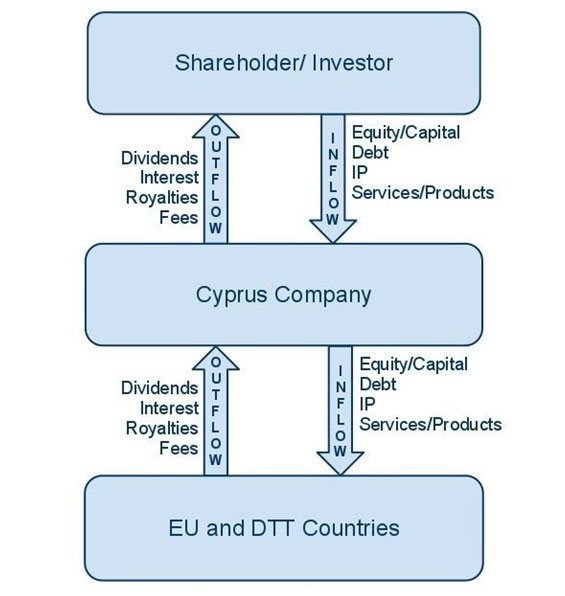

The Cyprus Company – Basic Ideas for Structuring

Considerations

The basic features behind any structuring with a Cyprus company are the treatment of:

1. Investment/Equity/Capital vis a vis Dividends

2. Debt / Loans vis a vis Interest / Capital Repayment

3. Intellectual Property / Licensing vis a vis Royalties

4. Services Provision/ Product Supply vis a vis Fees & Price

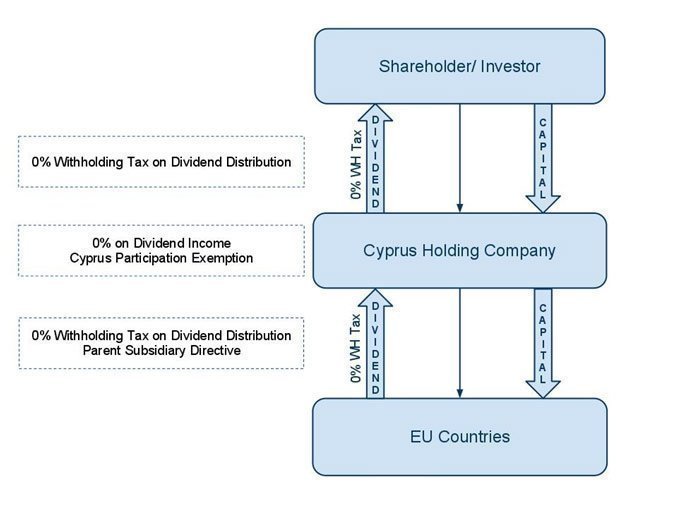

Cyprus Holding Company for EU

Reason

Establish a Cyprus Company to hold operating or non-operating European Union Subsidiaries.

Take Advantage

- No Thin Capitalization issues;

- Cyprus Participation Exception (No tax on dividend income from subsidiary);

- No Withholding Tax on dividends for the Subsidiary (EU Directives);

- No Withholding Tax on dividends from Cyprus Holding to the Investor / Shareholder

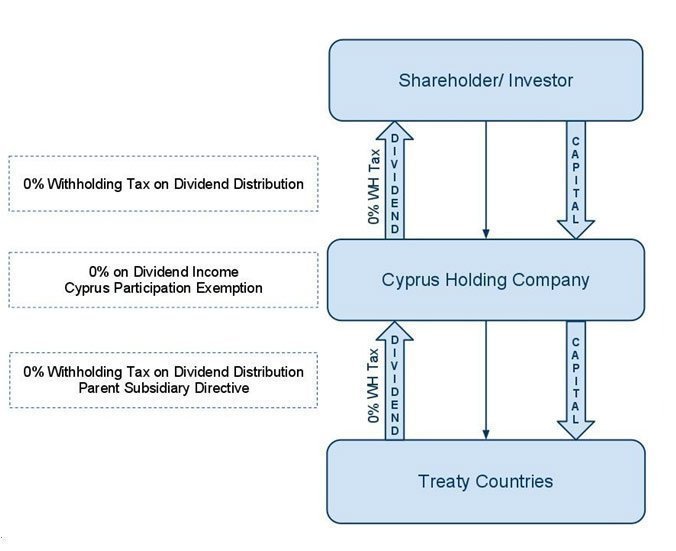

Cyprus Holding Company for Treaty Countries

Reason

Establish a Cyprus Company to hold operating or non-operating Treaty Country Subsidiaries.

Take Advantage

- No Thin Capitalization issues;

- Cyprus Participation Exception (No tax on dividend income from subsidiary);

- No or Low Withholding Tax on dividends for the Subsidiary (Double Tax Treaties);

- No Withholding Tax on dividends from Cyprus Holding to the Investor / Shareholder

Cyprus Finance Company

Reason

Establish a Cyprus Company to finance operations of an EU – Treaty Operations Company.

Take Advantage

- All advantages of Cyprus Holding Companies;

- No or Low Withholding Tax on Interest for the Subsidiary (Double Tax Treaty or EU Directives);

- No Withholding Tax on dividends from Cyprus Holding to the Holding Company.

- Interest Margin taxable in Cyprus at 12.5%

Cyprus Royalties Company

Reason

Establish a Cyprus Company to license intellectual property (IP) to an EU/Treaty Company.

Take Advantage

- 80% exemption of IP related net income (based on conditions);

- No or Low Withholding Tax on Royalties for the Subsidiary (Double Tax Treaty or EU Directives);

- No Withholding Tax on dividends from Cyprus Holding to the Holding Company.

- No Withholding Tax on royalties from Cyprus Royalties to the Foreign Royalties Company.

Cyprus Holding Company for Real Estate Single Tier

Reason

Establish a Cyprus Holding Company to hold Subsidiaries with Real Estate in EU/Treaty Countries. Disposal of Company at Treaty Country Level.

Take Advantage

- No Capital Gains or Disposal Tax at Treaty Country either due to Double Tax Treaty protection or due to local legislation.

- No Tax in Cyprus upon disposal of shares in Treaty Company.

Cyprus Holding Company for Real Estate Two Tier

Reason

Establish a Cyprus Holding Company to hold Subsidiaries with Real Estate in EU/Treaty Countries. Disposal of Company at Cyprus Level.

Take Advantage

- No Disposal at Treaty Country.

- No Tax in Cyprus upon disposal of shares in 2nd Cyprus Company.

Cyprus Securities/Titles Trading Company

Reason

Establish a Cyprus Company to hold and trade securities or “Titles”.

Take Advantage

- Full Tax Exemption in Cyprus.

- Dividend Income exempt in Cyprus. (subject to conditions)

- Interest income taxable at 12,5% deducting expenses (active interest)

Disclaimer: All of the proposed structures above are generic samples and cannot be applied without detailed analysis of the real case scenario. Application of those structures before prior consultation is not advised.

ABOUT REANDA CYPRUS LIMITED

Reanda Cyprus Limited is a Cyprus based audit firm licensed and regulated by the Institute of Certified Public Accountants of Cyprus (ICPAC). The Firm is the Cyprus member firm of Reanda International, an international network of independent accounting and consulting firms, China's first professional accounting network to collaborate with independent member firms from overseas countries and regions. These member firms provide assurance, tax consulting and specialist business advisory to privately held business and transnational conglomerates.

Our firm has also established relationships and associations with some of the most respected professional services firms all over the world, which allows us to provide holistic solutions to our clients’ needs on a global scale.

Our qualified and high caliber team, the membership in Reanda International and our network of experienced associated professionals guarantee the provision of a comprehensive range of professional services for both local and international companies.

The Firm was established to provide high quality services to its clients and assist in maximising their results. Full commitment to our clients by satisfying their needs is the core objective of our organisation. Our mission is to continuously add value to our clients through the provision of the highest quality professional services on a timely and cost effective basis.